Economic Substance

Regulations in UAE. Are you ready to notify of your compliance?

The UAE introduced

Economic Substance Regulations to honour the UAE’s commitment as a member of

the Organisation for Economic Co-operation and Development (OECD) Inclusive

Framework on BEPS (Base Erosion and Profit Sharing), and in response to a

review of the UAE tax framework by the EU which resulted in the UAE being

included on the EU list of non-cooperative jurisdictions for tax purposes (EU

Blacklist). The issuance on 30 April 2019 of the UAE Cabinet of Ministers

Resolution No.31 of 2019 concerning Economic Substance Regulations (the “Regulations”),

and the subsequent release of the Guidance on the application of the

Regulations (Ministerial Decision No.215 of 2019) on 11 September 2019, was a

requirement for the removal of the UAE from the EU Blacklist on 10 October

2019. The purpose of the Regulations is to ensure that UAE entities that

undertake certain activities (called “Relevant Activities”) are not used to

artificially attract profits that are not commensurate with the economic

activity undertaken in the UAE.

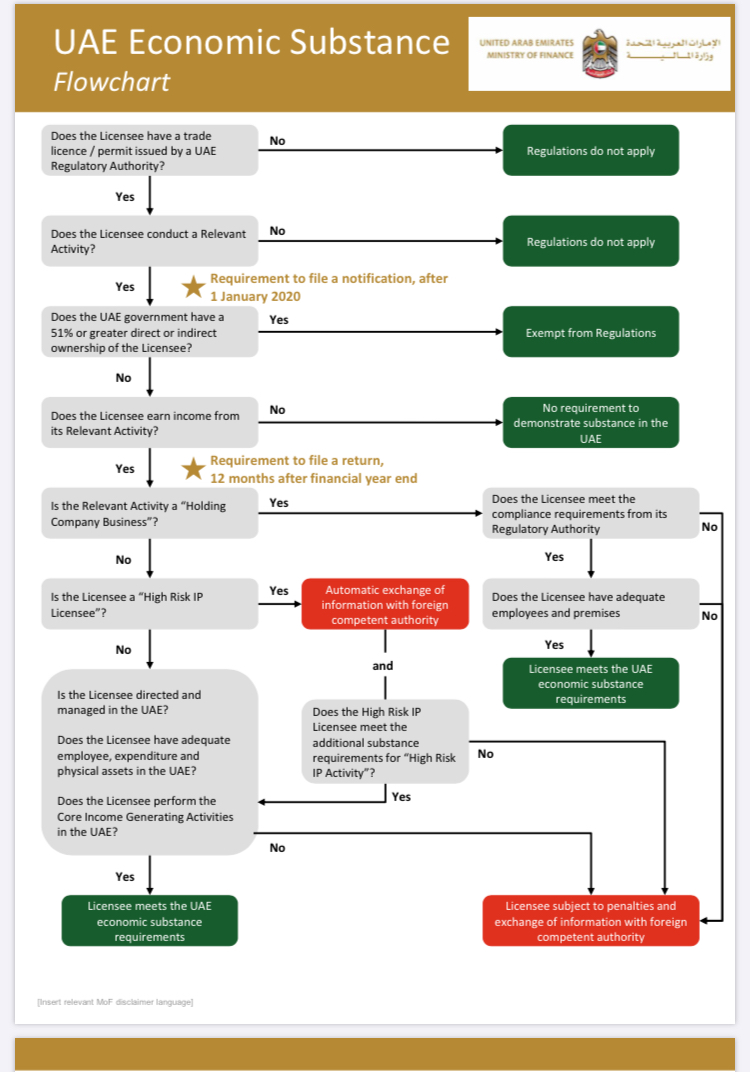

The Regulations

require UAE onshore and free zone companies and other UAE business forms that

carry out any of the “Relevant Activities” listed below to maintain an adequate

“economic presence” in the UAE relative to the activities they undertake.

Relevant

Activities:

The Regulations

provide a definition to each of the above Activities. The provisions of the

Regulations shall not apply to Companies in which the Federal Government of the

UAE or the Government of any Emirate of the UAE, or any governmental authority

or body or any of them has at least 51% direct or indirect ownership in their

share capital.

The Regulations

apply to financial years commencing on or from 1 January 2019. Entities will

need to submit a notification to their Regulatory Authority (defined under

Cabinet Decision No (58) of 2019 issued on 4 September 2019) from 1 January

2020 onwards, and prepare and submit to the same Regulatory Authority an

economic substance declaration within 12 months from the end of their

financial year (e.g. 31 December 2020 for entities with a financial year ending

31 December 2019). Current notification is for financial year from 1 January

2019 until 31 December 2019. In particular, the free zone entities are required

to submit economic substance notifications to a relevant Free Zone Authority an

many of them set up a deadline for submission of such notification is 30 June

2020 (DIFC, DMCC, Ras Al Khaimah, DAFZA, etc).

As per Clause 8 of Regulations,

the Licensee shall submit to the Regulatory Authority a Notification

confirming;

a) Whether or not

it carries out a Relevant Activity;

b) Whether or not

all or any part of the Licensee’s gross income in relation to a Relevant

Activity is subject to tax in a jurisdiction outside the UAE; and

c) The date of the

end of its financial year.

Whilst the commercial license may

indeed state the Relevant Activity, a ‘substance over form’ approach must be

used to determine whether a Licensee undertakes a Relevant Activity and is

within the scope of the Regulations. This means looking beyond what is stated

on the commercial licence to the activities actually undertaken by the Licensee

during a financial period.

Failure by an

entity to comply with the Regulations shall result in administrative penalties

(for example, failure to notify can trigger a penalty from AED10,000 until

AED50,000), spontaneous exchange of information with the Foreign Competent

Authority and potential suspension, revocation or non-renewal of its registration.

For each financial period in which a

Licensee earns income from a Relevant Activity, it will need to meet an

Economic Substance Test in relation to that activity. The Economic Substance

Test requires a Licensee to demonstrate that:

? the Licensee and Relevant Activity

are being directed and managed in the UAE;

? the relevant Core Income Generating

Activities (CIGAs) are being conducted in the UAE; and

? the Licensee has adequate

employees, premises and expenditure in the UAE.

The UAE Ministry of Finance

recommends the following non-exhaustive list of matters a Licensee should

consider (and action, where relevant) to comply with Economic Substance

Regulations:

? Assess what (if any) Relevant

Activities it has performed during the financial period (applying a “substance

over form” approach);

? Assess the amount and type of

income earned (if any) from the Relevant Activity during the financial

period;

? Hold board meetings with a quorum

of directors physically present in the UAE;

? Ensure board meeting minutes are

signed and maintained in the UAE;

? Identify the amount and type of

expenses and UAE based assets (incl. premises) in respect of the Relevant

Activity, and ensure access to assets (incl. premises) can be demonstrated

(through agreements and financial records)

? Identify the number of UAE based

full-time employees or other personnel (and their qualifications) responsible

for carrying on the Licensee’s Relevant Activity; and

? Ensure control and supervision over

any outsourcing arrangements can be demonstrated, e.g. through contractual

agreements.

Additional actions may be required to

ensure a Licensee can demonstrate sufficient economic substance in the UAE for

a relevant financial period, and the considerations above may differ where a

Licensee has either a Holding Company or a High Risk IP Business. ?????